Deep Dive with Lyazzat Borankulova, Managing Director for Strategic Development of Samruk-Kazyna

Posted on 12/16/2020

This is a deep dive interview with Lyazzat Borankulova, Managing Director for Strategic Development of Samruk-Kazyna.

General information about Samruk-Kazyna

The sovereign wealth fund Samruk-Kazyna (the Fund) was founded in 2008 as a holding company by the decree of the President of Kazakhstan and is currently within the Top-20 global sovereign wealth funds in terms of the value of assets under management. The main mission of the Fund is to preserve and create wealth for future generations, with the government of Kazakhstan being the sole shareholder. By the end of 2019, the total assets under management of Samruk-Kazyna stood at over US$ 69 billion, comprising systematically important companies in oil & gas, mining, transportation, power, telecom, postal, chemicals, and real-estate sectors of Kazakhstan, with domestic market share ranging from 26% to 100%. We are currently a member of the International Forum of Sovereign Wealth Funds, complying with Santiago Principles and scoring 10-possible points on the Linaburg-Maduell Transparency Index published by SWFI. Samruk-Kazyna plays a pivotal role in Kazakhstan’s economic development, acting as a vehicle in attracting investments, introducing and implementing advanced technologies and driving operational efficiency of its portfolio companies.

This interview will appear in the upcoming issue of the Sovereign Wealth Quarterly.

Michael Maduell, President of the Sovereign Wealth Fund Institute (SWFI): Thank you, Ms. Borankulova, for the opportunity to learn more about the current macroeconomic situation in Kazakhstan and developments within Samruk-Kazyna. The Covid-19 pandemic has jolted the foundations of economies globally. First, can you share with our audience of institutional investors how Kazakhstan’s economy was affected by the Covid-19 pandemic?

Lyazzat Borankulova, Managing Director for Strategic Development of Samruk-Kazyna: The Covid-19 pandemic caused tremendous human and economic hardship across the world, and Kazakhstan is not an exception. The virus and the measures taken to protect public health induced sharp declines in economic activity, a surge in job losses, weakening of exchange rate, and acceleration of inflation.

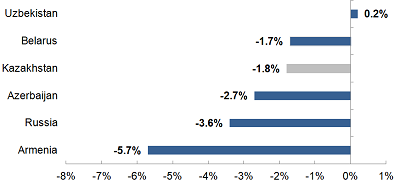

Real GDP growth in selected CIS countries YoY, 1H2020

Source: Committee on statistics of Kazakhstan, Bloomberg

Strict lockdown measures since the beginning of April and the collapse in oil prices significantly affected Kazakhstan’s economic activity. Over 1H2020, Kazakhstan’s real GDP weakened by 1.8% YoY, mostly impacted by sectors directly exposed to lockdown measures such as retail & wholesale trade and transportation, while industrial production has been sustainable, expanding by 3.2% YoY. However, Kazakhstan’s economy has been more resilient compared to other CIS countries, with Armenia, Russia and Azerbaijan real GDP declining by 5.7%, 3.6% and 2.7%, respectively.

Kazakhstan’s YoY GDP growth %

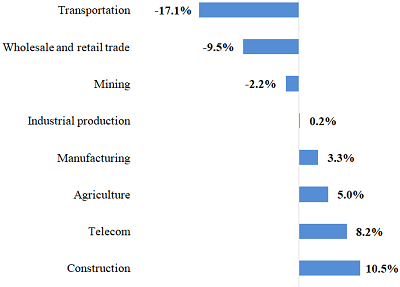

Real growth by sector YoY %, 9M2020

Source: Committee on statistics of Kazakhstan

Growth in manufacturing (+3.3% YoY), agriculture (+5.0% YoY), construction (+10.5% YoY) and telecom (+8.2% YoY) partially offset the negative performance of wholesale & retail trade (-9.5% YoY) and transportation (-17.1% YoY), resulting in 9M2020 real GDP contracting by 2.8% YoY. The mining output was undermined by Kazakhstan’s compliance with the OPEC+ deal, while the increase in manufacturing was broad-based and driven mostly by automobile production (+51.6% YoY), pharmaceuticals (+39.8% YoY), machinery (+16.6% YoY), and light industry (+14.1% YoY).

Recent updates from the Ministry of National Economy indicate greater ability of Kazakhstan’s economy for recovery, as the country’s real GDP is expected to decline by just 2.1% in 2020. Current recovery of oil prices up to the level of 50 USD per barrel will definitely support GDP improvement until year-end.

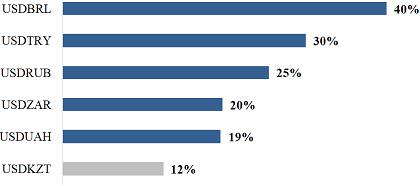

Affected by high oil price volatility amidst global demand contraction and Saudi Arabia-Russia price war, tenge weakened by more than 12% over 9M2020. However, compared to other emerging market currencies, the USD/KZT exchange rate has been more resilient, demonstrating less volatility, compared to rouble and lira.

Developing countries exchange rate dynamics, 9M2020

Source: National Bank of Kazakhstan, Bloomberg

Michael Maduell: How did Kazakhstan’s government respond to the crisis?

Lyazzat Borankulova: Kazakhstan’s government took broad and forceful actions to support economic activity and aggregate demand. The total fiscal stimulus package amounted to approximately 9% of GDP and aimed to cover additional unemployment benefits, infrastructure and housing construction, and direct financing to combat the Covid-19 spread. In addition, our government also introduced a number of non-monetary stimulus measures, including temporary cancelation of taxes and easing of regulatory burdens for businesses in services, mining and transportation sectors.

We would like to note that the recovery of Kazakhstan’s economy, as well as the global economy, will depend heavily on the course of the virus. The ongoing public health crisis will weigh on economic activity, employment, and inflation in the near term and poses substantial risks to the economic outlook over the medium term until an effective and available vaccine is introduced. For 2021 to 2025, we expect Kazakhstan’s real GDP growth to average at 4%, underpinned by the low-base effect, anticipated recovery in oil prices, higher real GDP growth of Kazakhstan’s main trading partners, and significant fiscal stimulus.

Michael Maduell: Let’s dive down a little deeper. Can you shed some light on the performance of Samruk-Kazyna and its portfolio companies that were impacted by the pandemic?

Lyazzat Borankulova: Pre-pandemic period has been exceptional for our financial performance. Between 2015 and 2019, the Fund’s net asset value (NAV) grew by more than 45%, driven by the above-average profitability of our portfolio companies. In 2019, Samruk-Kazyna generated 8.6% ROACE, while our consolidated EBITDA stood at KZT2.364tln with a 22.1% EBITDA margin. In 2018, the Fund’s consolidated net income for the first time exceeded KZT1 trillion, with 2019 net income being even higher at KZT1.243 trillion, supported by the management’s actions to optimize and restructure portfolio companies and higher commodity prices.

In 2020, our operating and financial performance has been undermined by the Covid-19 pandemic too with underperformance in transportation and oil & gas assets being partially offset by strong performance in mining and telecom assets. To mitigate the pandemic impact, we took additional efforts to restructure our portfolio companies, optimized our operating expenses, and revised capital expenditures. The measures that have been taken to mitigate impact of external factors supported the Fund’s 2020 financial performance. We expect to outperform our initial 2020 financial plans. In particular, consolidated net income and ROACE are estimated to exceed business plan assumptions by 156% and 0.6 percentage points, respectively, supported by higher oil prices and more favourable macroeconomic environment. Systematic supportive measures allowed to receive in June the S&P rating agency confirmation of the long-term and short-term credit ratings of Samruk-Kazyna at the level of BB + / B, with a stable outlook.

We were also honored to see our CEO Akhmetzhan Yessimov within The Public Investor-10 ranking of the most significant and impactful asset owners and public executives recently published by SWFI. We see this as recognition of Samruk-Kazyna’s efforts to support the performance of our portfolio during the difficult and pandemic year of 2020.

Michael Maduell: Now, let’s turn to the developments within Samruk-Kazyna. Last time, the CEO of the Fund mentioned that Samruk-Kazyna adopted a New Development Strategy and currently undergoing a transformation to an investment holding. Any updates on progress?

Lyazzat Borankulova: Until 2020 inclusive, the Fund focused its attention and resources on improving the efficiency and profitability of its portfolio companies to create the foundation for further growth, successful transfer to a competitive environment, and transition to the next stage of the Fund’s investment portfolio development.

The transition of the Fund into an investment holding by 2024 complies with the Development Strategy of Samruk-Kazyna for 2018-2028 adopted in 2018 and the Fund’s Management Council recently approved The Concept of Transition to Investment Holding. The expected changes will significantly affect the operating model of the Fund, with the transition from operating to investment holding entailing substantial revision of our investment activities.

In 2021, we will continue restructuring our current portfolio of investments, finalizing the process of transferring the Fund’s assets into a competitive environment, initiated by the Sole Shareholder, and will initiate the divestment from the current portfolio with the subsequent reinvestment of these funds into new investments domestically and abroad. A full transition to active management of the investment portfolio and an investment holding business model is planned to be finalized not later than 2024.

In 2021, Samruk-Kazyna plans to amend the Dividend Policy in relation to the Sole Shareholder, which will provide a mechanism of distribution of dividends received from the portfolio between the Sole Shareholder and the Fund, providing us with more flexibility to reinvest available funds into new investments.

The process of transferring large assets to a competitive environment through IPO and sale to strategic investors is expected to be completed by 2024. Currently, Kazpost and Samruk-Energy are planned for sale in 2021, while NC KazMunayGas, Air Astana, Tau-Ken Samruk, and Qazaq Air are planned for sale in 2022, with NC Kazakhstan Temir Zholy in 2023. Offering stake and implementation mechanisms will be determined closer to timing of the transactions. For large assets, the first part of offering stake will be sold under the transfer to a competitive environment, while the remaining shares will be offered within the framework of the Fund’s own divestment program.

Until 2028, Samruk-Kazyna will gradually divest from its legacy assets, with the pace and timing of divestment premised on favorable capital market conditions, new investment opportunities, and overall portfolio return. The Fund plans to retain controlling ownership stakes in large strategic assets, such as NC KazMunayGas, Kazatomprom, NC Kazakhstan Temir Zholy, Kazakhtelecom, and KEGOC, while up to 100% of stakes in non-strategic portfolio companies will be considered for divestment. To achieve the Fund’s primary goal of increasing overall portfolio return, the assets will be divested in stages, with high-yield assets replacing assets with a low investment return.

It was agreed with our Sole Shareholder that 50% of proceeds from the sale of assets to the competitive environment and all divestment proceeds will be directed to new investments of the Fund. Meanwhile, pipelines for potential private and public investments and assets for M&A deals will be worked out and formed. The main goal of active portfolio management is to increase the portfolio’s profitability over the long run.

During the period of economic difficulties in the country arising from the pandemic and low oil prices, the Fund will focus on investments and attraction of direct investments in non-resource sectors Kazakhstan’s economy via the active use of co-investment instruments. The basic criteria for new investments are to ensure diversification of the Fund’s current portfolio and investment return exceeding the cost of equity.

The Fund intends to make direct investments both domestically and abroad together with partners, sovereign wealth funds, and institutional investors using various co-investment mechanisms, including through entry into private equity funds. Meanwhile, our public investments will be carried out both independently and by attracting external asset managers. As favorable market opportunities arise, the Fund’s portfolio will be diversified in terms of geography, increasing the dollar-denominated proceeds from international investments and reducing portfolio volatility over the long term.

Michael Maduell: It is fascinating to see the gradual shift from a holding company to a sovereign fund building out a savings pool for investment diversification. Could you please provide more details about how public investments will be implemented? Will you have any particular focus on regions or asset classes?

Lyazzat Borankulova: Public investments will mainly be implemented under our Future Generations Fund (FGF) mandate. FGF is designed to accumulate and generate income for future generations through investments into publicly-traded asset classes as well as international private investments.

The Fund expects that, on average, approximately 25% to 30% of overall international investments will be represented by public investments to diversify the Fund’s portfolio not only by geography but also by asset classes. The structure will be balanced with a moderate level of risk, close at the initial stage to the conservative level in developed countries, with a gradual increase of equity allocation.

Michael Maduell: And what about international private investments. How do you see this playing out?

Lyazzat Borankulova: International private investments will be initiated over the medium term in sectors that are strategically linked to Kazakhstan, except for the oil and gas industry. I highlight that, initially, our private investments will be concentrated in Kazakhstan to support the development and diversification of the country’s economy. Consequently, the target sector range may change depending on domestic macroeconomic conditions and the emergence of favorable market opportunities globally. Over the long run, until 2028, the share of international investments, both private and public, is expected to rise to at least 4% and at most 20% of the net asset value of the Fund’s portfolio. We prefer to implement co-investments with private companies, corporations, including within the framework of G2G intergovernmental agreements, as well as with other sovereign funds.

Michael Maduell: In what companies and industries will you invest domestically?

Lyazzat Borankulova: The Fund is ready to cooperate with strategic investors to invest in commercially attractive projects (greenfield, brownfield) in the non-resource sectors of Kazakhstan.

When considering mutually exclusive projects, priorities for investment in Kazakhstan will be given to industries that meet the interests of the Fund and its Sole Shareholder. For now, we have identified 12 priority sectors, including healthcare, agriculture, manufacturing, logistics, machinery, information technologies, construction, green energy, chemicals, services (fintech), mining (rare-earth elements), science & research. This list is not exhaustive; we update the list on an annual basis when global and regional trends and markets change.

Michael Maduell: Sovereign wealth funds are known for forming unique partnerships from both the private sector and among peer sovereign investors. Can you share with us any deals on the domestic investments front?

Lyazzat Borankulova: Over the past year, Samruk-Kazyna attracted several investors and co-invested as a limited partner in two private equity funds, Eurasian Nurly Investment Fund and Da Vinci Emerging Technologies Fund III, with the total committed capital of approximately US$ 600 million. In addition, despite the escalating pandemic, in October 2020, we signed a partnership agreement for co-investments with Bpifrance, the French public investment bank, to launch €100 million investment platform dedicated to French and Kazakhstani companies, contributing to the development of trade and economic relations between the two countries. This bilateral investment platform will target French, Kazakhstani, or joint-venture SMEs and intermediate-sized companies operating in industrials, energy and environmental transition, agriculture, education, and healthcare.

Michael Maduell: What incentives will foreign investors have from co-investment with Samruk-Kazyna?

Lyazzat Borankulova: We intend to establish partnerships with leading sovereign funds and investment companies that have experience and technologies for joint implementation and financing of investment projects, creating new companies that will drive the structural transformation and diversification of Samruk-Kazyna’s portfolio. From our side, joint investment projects will benefit from Samruk-Kazyna’s domestic expertise, our established relations with the government of Kazakhstan as a Sole Shareholder, size and significant role in Kazakhstan’s economy, and possible synergy benefits with our portfolio companies. We welcome all potential investors and partners and value their experience, competitive edge in know-how and technology, best practices, and performance-oriented culture.

Michael Maduell: Thank you for your time and giving us an update. To learn more about Samruk-Kazyna, please visit, http://sk.kz/en

SWFI ranking of sovereign wealth funds by total assets size

Source: SWFI